Online Protection Alert

Please note that we will only make contact with you if you are already a client of ours or if you have reached out to us for assistance.

Welcome to

Debt Relief Solutions

Debt Relief Solutions (CIC) Ltd

Debt Relief Solutions is a Community Interest Company which is run on a not for profit" basis.

This means that the company does not make any profits. We think that this sits in with our company ethos and believe that any organisation offering debt advice and education should not make a profit from other people's misfortune.

Many people are still living with unstable finances post-covid.

Get your hands on our FREE download with top tips for managing your money during this difficult time.

Welcome!

We are overjoyed that you have popped over to say hello and are ready to help you with whatever financial problem you are facing.

Whatever your problem, we can help. You may be unable to repay your debts due to loss of income caused by illness, redundancy or relationship breakdowns or have got into financial difficulty due to covid-19. We can certainly help by providing a solution to suit your circumstances and taking away the worry and stress.

Whatever the reason you are visiting our website, we have lots of information and advice for you, please check out our freebies where you can gain lots of knowledge and tips to help you. Just one other thing, we are a "not for profit" Community Interest Company, which means that we don't believe that organisations should be making money from other peoples misfortunes (and believe us there are lots of them that do!).

So if we can help you, why not give us a call, and let us deal with the burden.

Tel: 0333 240 0851

helping

Your Guides on the Journey

We are the helping hand you may need to get you back in a place of financial freedom. Having money problems is no fun, we want to work with you and help you to overcome your financial burdens.

Come on in and see who we are, and why we love what we do.

WHAT DO WE DO?

We have a number of different solutions to help with your financial situation.

EMERGENCY ASSISTANCE

Can we help you with a really urgent situation? Pop in here and we will call you right back.

WHAT DO WE DO?

We have a number of different solutions to help with your financial situation.

EMERGENCY ASSISTANCE

Can we help you with a really urgent situation? Pop in here and we will call you right back.

Three Little Words

There are three little words that we have adopted which sums us up perfectly.

CARE ♦ SUPPORT ♦ COMPASSION

See what Pauline from Birmingham had to say about us below...

"I felt such a relief when I spoke with DRS, they were compassionate, kind and very professional. My debts are under control and I have never felt better."

support

Our Services

We can help with:

- Debt Intervention

- Debt Counselling

- Debt Education

- Debt Management

We offer:

- Freebies

- E-Courses

- Partnerships

support

Our Services

We can help with:

- Debt Intervention

- Debt Counselling

- Debt Education

- Debt Management

We offer:

- Freebies

- E-Courses

- Partnerships

If you have an urgent financial problem we can intervene on your behalf to take away the pressure. We can help to set up a debt management plan, an easy way to deal with your creditors each month at a level which you can afford. If you are worried or stressed about money matters, then have a chat with us and we will share the burden.

We offer a range of workshops, seminars and classes to teach you how to manage your money more effectively. We love working together with many organisations to provide financial wellbeing in the community, so get in touch if you need any of the above or would like to partner with us.

Want to get on top of your finances?

Why not make a start by getting hold of our FREE Financial Self-Assessment Sheet. By using this tool you will see that by making small changes you can regain control of your finances.

TESTIMONIALS

GARY

We were struggling managing our debts and being self employed with variable income only made things worse. Thankfully working with DRS we have been able to make regular affordable repayments to suit our pocket knowing that we will one day be debt free.

JANE

Since my separation I found I was unable to manage my money and my debts were spiralling out of control. DRS have been a rock for me and my family and we feel so much happier knowing we can call them any time for help when needed.

BILL & SUE

A real weight was lifted right from the first call, now we are able to see the light at the end of the tunnel. It's going to take a while, but we are confident that with the help of DRS things are already improving.

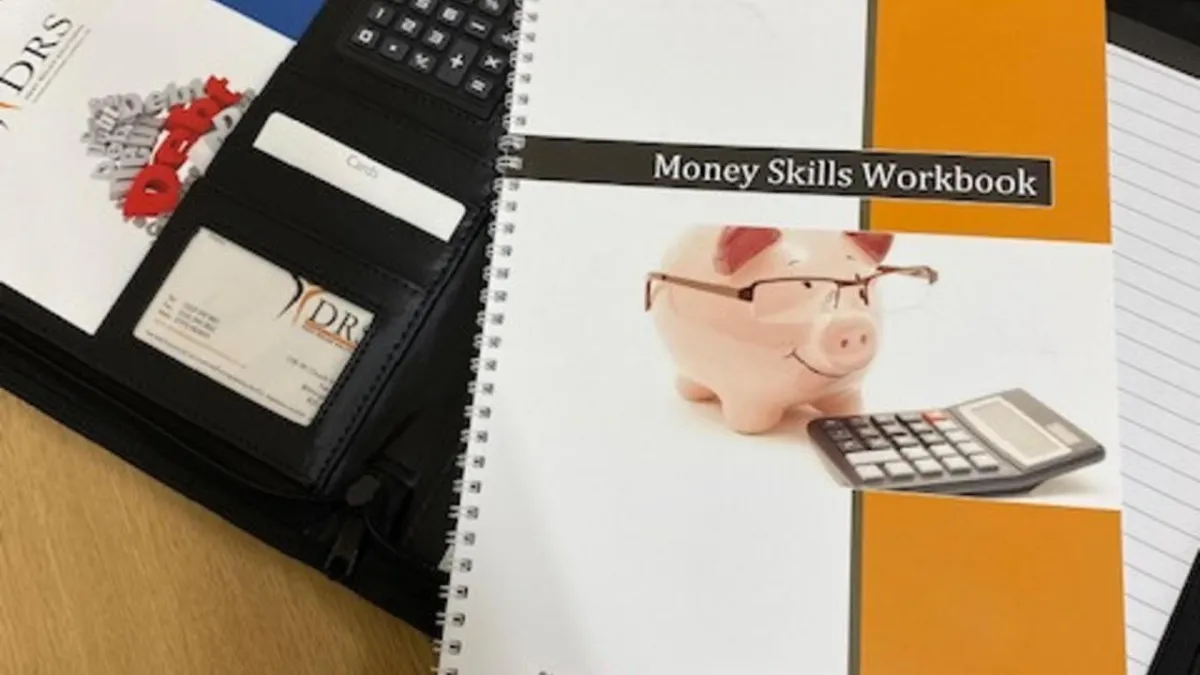

Get The Money Skills Workbook Pack

If you need to identify where your money is going and where savings could be made to make life easier, then this pack is ideal for you.

The workbook deals with debts and how to manage them along with what happens when third parties get involved. Having said that, even if you are not struggling with debt at this time, there is lots of useful information which can prepare you for anything in the future.

Just imagine now fabulous it would be to finally get your finances back under control. We will send you a full pack including zipped wallet containing the workbook for you to work through at home at your own pace. The workbook will ask you lots of questions and by completing each section you will be performing your own financial review.

DIVE INTO OUR BLOGS

Planning for The Future

What steps have you taken to plan for your future? Have you taken out a pension? Set up a savings account? Or have you made other plans?

When you are young it's difficult to even think about buying a pension but in actual fact, the earlier you start the better.

The longer you have to invest in a pension the more you will have paid out to you when you retire, it's simple really.

Of course, planning for the future doesn't just involved pensions. We have to plan for many things. One of those can be planning for when your benefit payments end. This is the case especially with something like Child Benefit which pays out until the child reaches the age of 18 or leaves full time education. So it makes sense to plan for when the time comes that you no longer receive this benefit.

What can you do then? Well, to start with calculate when the payment is due to end and work backwards. For example, if you only have two years left, then you should calculate how much you will be short per month after the two year period and start by looking at either increasing your income, perhaps by working more hours, or taking on an additional part time job, or by decreasing your expenses a little each month.

It could be that your child will be leaving home at that time, so some of your regular household expenses will be automatically reduced anyway. You can take this into account when making your calculations.

So why not take out some time now and see what you need to plan for and how you can make a gradual transition in order to avoid a sudden income loss jolt when the time comes.

DIVE INTO OUR BLOGS

Planning for The Future

What steps have you taken to plan for your future? Have you taken out a pension? Set up a savings account? Or have you made other plans?

When you are young it's difficult to even think about buying a pension but in actual fact, the earlier you start the better.

The longer you have to invest in a pension the more you will have paid out to you when you retire, it's simple really.

Of course, planning for the future doesn't just involved pensions. We have to plan for many things. One of those can be planning for when your benefit payments end. This is the case especially with something like Child Benefit which pays out until the child reaches the age of 18 or leaves full time education. So it makes sense to plan for when the time comes that you no longer receive this benefit.

What can you do then? Well, to start with calculate when the payment is due to end and work backwards. For example, if you only have two years left, then you should calculate how much you will be short per month after the two year period and start by looking at either increasing your income, perhaps by working more hours, or taking on an additional part time job, or by decreasing your expenses a little each month.

It could be that your child will be leaving home at that time, so some of your regular household expenses will be automatically reduced anyway. You can take this into account when making your calculations.

So why not take out some time now and see what you need to plan for and how you can make a gradual transition in order to avoid a sudden income loss jolt when the time comes.

Give us a call or pop in & see us, the kettle is always on!

If you need help, want to learn more about what we do, or just want a chat about your circumstances, we would love to hear from you.

Give us a call, send us an email, or pop in.

Debt Relief Solutions (CIC) Ltd

Authorised and Regulated by the FCA FRN: 625583

181 Church Road, Yardley, Birmingham B25 8UR Tel: 0333 240 0851 (local call rate)

Email: wills@robertshawandco.co.uk

© 2023 Debt Relief Solutions (CIC) Ltd